Summary

Many definitions, one goal:

Promoting a performant product lifecycle while protecting the environment and ensuring people’s welfare

At Amundi, we consider that the Circular Economy is a change of economic model that allows to produce sustainable consumer goods, while protecting nature - by giving it time to regenerate - and ensuring the well-being of individuals.

This new economic model translates into:

- A better management and use of natural resources;

- Goods designed and produced to last;

- Consumers who are informed about the environmental impacts of what they buy and who consume sensibly, and

- A more efficient system for processing end-of-life products from which more secondary raw materials can be obtained.

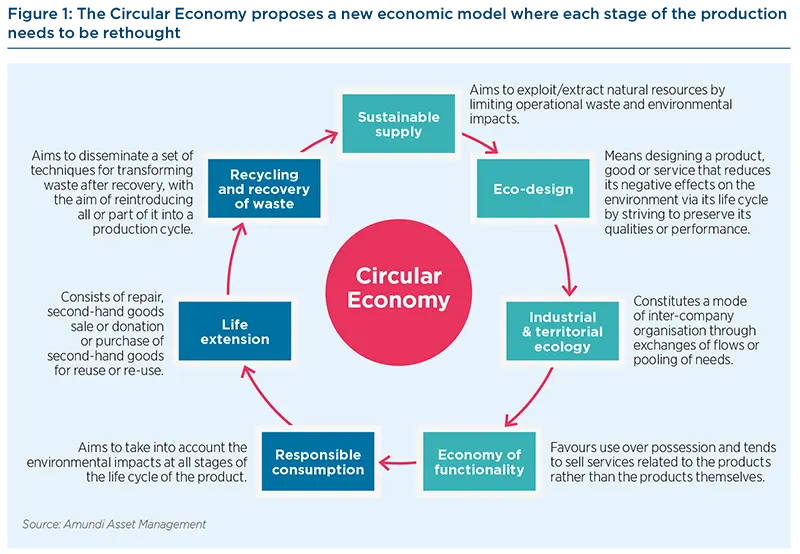

Each stage of the production of a product or a consumer good must therefore be reviewed in the light of this definition.

The concept of Circular Economy is constantly evolving and there is no universal definition. The definition we have chosen at Amundi is based on studies by Ademe, the Ellen MacArthur Foundation and the European Commission.

Each of these organizations propose different visions of the Circular Economy and put forward distinct characteristics of it. However, they agree on the need to limit the impact of human activities on nature.

Ademe has a systemic vision of the Circular Economy since, for it, it is above all a matter of inventing a new economic model whose primary objective is to reduce the environmental impact of the goods and products that human societies use while allowing them to increase their well-being.

The Ellen MacArthur Foundation, on the other hand, has a vision centered on the protection of nature and focuses on the fact that the Circular Economy must be restorative and regenerative by design, by limiting the production of waste and/or recycling it to make new products.

The European Commission, on the other hand, has an economic vision and is interested in maintaining the market value of products throughout their life, especially through the market value of recycled materials that are integrated into new products.

|

“The Circular Economy can be defined as an economic system of exchange and production that, at all stages of the product life cycle (goods and services), aims to increase the efficiency of resource use and decrease the impact on the environment while developing the well-being of individuals.” “A Circular Economy is based on the principles of designing out waste and pollution, keeping products and materials in use, and regenerating natural systems.1 ” “In a Circular Economy, the value of products and materials is maintained for as long as possible. Waste and resource use are minimised, and when a product reaches the end of its life, it is used again to create further value.2” |

Understanding why we must shift from a linear to a circular model is key for our future. Hard law is being introduced in many countries, especially in the EU and is going to change the way companies can produce and sell their goods over the next decades. We live in a world with finite materials and natural resources and we cannot keep wasting them as we do with the linear model because either we will face shortages in natural resources or we will put too much pressure on the environment, without which humans cannot live as we all depend on nature services. Besides, production of goods and land management represent 40% of CO2 emissions and Circular Economy, in particular through eliminating waste, reusing products and components and recirculating materials, can contribute to limit global warming to 1.5°C by 2100, in accordance with the Paris Agreement.

Why our economic model must be changed now?

Legislation is pushing to establish a Circular Economy, especially in Europe

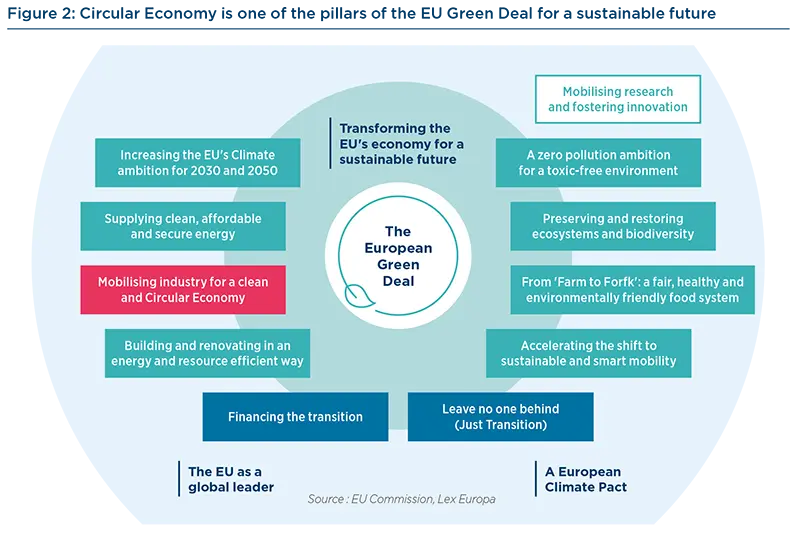

The European Union (EU) is committed to being a carbon neutral continent by 2050 and to decoupling economic growth from resource use. This commitment stems from a simple fact: climate change and environmental degradation are an existential threat to Europe and the world. The EU needs to accelerate the transition towards a regenerative growth model that allows nature to be restored, needs to maintain its resource consumption within planetary boundaries, and therefore manages to reduce its CO2 footprint and double its circular material use rate by 2030.

In order to achieve this commitment, the EU has embarked on a major economic overhaul, entitled “The European Green Deal” and based on the following elements:

One of the key elements of this economic transformation is based on mobilizing the industry for a clean and Circular Economy, through the New Circular Economy Action Plan adopted in March 2020.

The objectives of this new action plan are:

- Designing sustainable products: make sustainable products the norm in the EU, which means that products will have to last longer, be easily reused, repaired and recycled and at the same time made, as much as possible, of secondary raw materials;

- Empowering consumers and public buyers through better disclosure on the sustainability characteristics of the products;

- Implementing circularity in production processes by focusing on the seven resource intensive sectors and where the benefit from circularity is the most important, through an improved recycling rate allowing an increase in the quantity and the quality of secondary raw materials

This action plan focuses in particular on seven resource-intensive sectors, which are Electronics and ICT, Batteries and vehicles, Packaging, Plastics, Textiles, Construction and buildings, Food, water and nutrients.

The New Circular Economy Action Plan marks a turning point in the definition of Circular Economy. The 2015 European Circular Economy Roadmap focused specifically on recycling and waste treatment. The 2020 New Circular Economy Action Plan is no longer only about waste treatment or recycling but is defined as a whole new model in which every step of the production process needs to be rethought. Recycling is only one pillar of Circular Economy at the same level as eco-design or life extension, etc.

This shift is illustrated by the fact that in February 2021 the European Parliament voted in favor of establishing a “right to repair” – which means that all new washing machines, hairdryers, refrigerators and displays – including televisions – sold in EU countries must be repairable for up to 10 years. Similar requirements were made in November 2019 for smartphones, laptops and other consumer electronics.

Consequently, the goal is clear: sustainability is the key word and all means can be used, such as eco-design, life extension, economy of functionality or recycling.

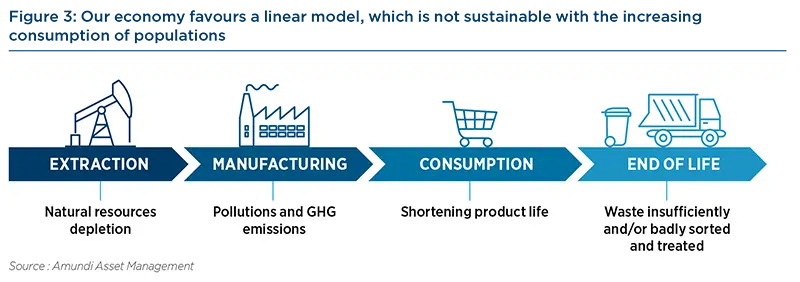

Creating a Circular Economy is a necessity as we live in a world with finite materials and natural resources while our linear model runs as if we had infinite resources and that we could keep taking and throwing away again and again.

We live in a world with finite materials even though we do not behave accordingly

The linear economic model we know today consists of extraction, production, consumption and disposal. Since the 19th century, economic growth has been based on an ever-increasing extraction of natural resources, a growing production of standardized goods, an ever-increasing consumption and renewal of these goods, and their disposal at the end of the race.

The extraction of natural resources includes both non-renewable resources, such as mineral raw materials and fossil fuels, as well as renewable resources such as air, water, soil or fauna and flora.

The demographic and economic explosion of the 20th century and the advent of mass consumption with cheap and easily replaceable products have put too much pressure on our environment and are now sounding the death knell of this linear economy.

Indeed, this linear economy has overlooked two important points: our natural reserves are limited and nature needs time to regenerate and make new resources available.

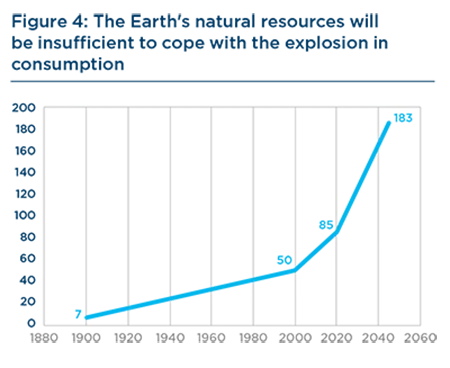

According to the Organization for Economic Cooperation and Development (OECD), the world population is expected to reach 9 billion people by 2050 and the global economy is expected to quadruple, resulting in an increasing demand for energy and natural resources.

In 1900, we consumed 7 Gt of raw materials worldwide, in 2000, we consumed 50 Gt (Krausmann, 2009) and in 2020, 85 Gt. Projections suggest 183 Gt in 2050 (UNEP, 2016). Our planet will not be able to respond to such an explosion of demand.

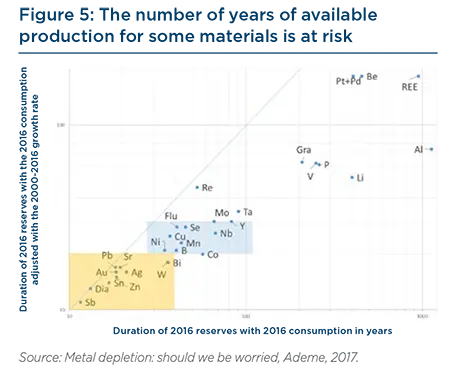

Indeed, according to scientific experts, at this pace of extraction, some raw materials will no longer be available in the next 50 years. In 2017, Ademe published a research paper saying that the “burnrate” indicator - which is the ratio between the known reserves (R) at a given time and the mine production (P) at that same time – was about to be reached for some materials and consequently that the number of years of available production for those materials are limited.

The figure above shows, for some minerals, on the x-axis the R/P ratio calculated for 2016 and on the y-axis the same R/P ratio but this time assuming that the growth in the consumption rate of mineral materials is not constant but continues to increase steadily and similarly to the period 2000-2016.

The mineral elements identified in the orange zone are those that could be in short supply in the next 20 years if demand continues to grow in the same way as between 2000 and 2016 and in the absence of new exploitable deposits (vs. between 10 and 40 years if we consider that future consumption is similar to that of 2016). The mineral elements concerned are antimony (Sb), diatimites (Dia), tin (Sn), zinc (Zn), gold (Au), silver (Ag), lead (Pb), strontium (Sr), wadalite (W).

The mineral elements identified in the blue zone are the minerals that we could run out of between 20 and 30 years. The mineral elements concerned are nickel (Ni), boron (B), bismuth (Bi), copper (Cu), manganese (Mn), cobalt (Co), selenium (Se), niobium (Nb), molybdenum (Mo), etc.

The metal with the lowest R/P ratio is antimony (Sb) with a shortage expected in 12 years. Antimony is increasingly used in lead-acid batteries for cars and as a flame retardant in plastics to replace bromine. At the other end of the spectrum, supply predictions for rare earths (REE), beryllium (Be), platinum (Pt) and palladium (Pd) exceed 200 years based on current known reserves.

The supply of certain minerals could therefore become a problem in the coming years.

|

RESOURCE DEPLETION OR SHORTAGE? It is important to distinguish between resource depletion and shortage. Resource depletion occurs when a resource is disappearing completely from the Earth's surface and cannot be renewed. In the case of mineral resources, resource depletion is unlikely: our knowledge of mineral reserves is still limited to the superficial part of the earth's crust and mining exploration allows the regular discovery of new deposits. The reserves exist but the question is whether exploitation of these reserves is possible, technically and economically. If we need to go deeper in the earth’s crust, the balance between the efforts (technical, human and financial) and the mineral use might be negative. If exploitation is not possible for technical or profitability reasons, we may then face a shortage situation. This shortage may be temporary (or not): the increase in the price of an ore or the discovery of new techniques may make the exploitation of certain deposits profitable. The shortage is therefore linked to market conditions rather than to the existence of the ore in nature. |

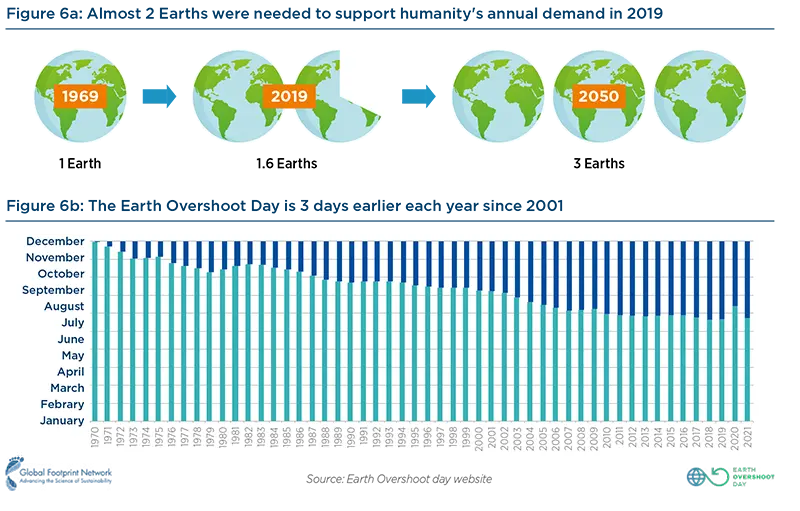

The same is true for renewable natural resources. The depletion of natural resources is pointed out every year by an NGO, The Global Footprint Network - which calculates the Earth Overshoot Day, which marks when humanity's demand for ecological resources and services in a given year exceeds what Earth can regenerate in that year. This is indeed the depletion of renewable resources, since we consume resources without giving them time to renew themselves, constantly reducing the available stock on Earth. The example of fishing illustrates this phenomenon very well: the industrial fishing carried out for several decades has led to 75% of fishery resources being fully exploited, already overexploited or heavily overexploited. This overexploitation leads to a decline in fish resources, as the fish do not have the time to reproduce quickly enough to counterbalance the effects of fishing. To stem this decline in fish stocks, moratoriums are imposed or bans are imposed when certain species are considered to be on the verge of extinction (this is the case for the whale, which has been a protected species since 1986). However, some specialists consider that it is too late for some species to be saved.

Since 1970, the world is in an ecological deficit. In 2019, Earth Overshoot Day3 was on July 29th, which means that 1.7 Earth planets were needed to support humanity's annual demand on the ecosystem versus only one planet in 1970. Since 2001, this date is moving on average 3 days earlier per year4. Should the global population reach 9.6 billion by 2050, the equivalent of almost three planets could be required to provide the natural resources needed to sustain current lifestyles.

Therefore, the linear model of producing more and more and throwing away large amounts of waste, without any recycling, is in contradiction with the planetary limits. The consumer society has finally given rise to a society of waste.

Global waste production was estimated to be 1.3 billion tonnes per year in 2012 vs 2.01 in 2018 (+55%) and is expected to grow to 3.40 billion tonnes by 2050 under a business-as-usual scenario (+160%)5. This high increase will come mainly from developing countries and continents (Asia and Africa).

Amongst these wastes, some are recyclables, such as paper, cardboard, plastic, metal and glass: they represent from 16% of waste streams in low income countries to 50% in high-income countries. Despite this high recyclable rate, only one-third of waste in the high-income countries is recovered through recycling and composting.

As of 2018, it is estimated that globally about 37% of waste is disposed of in some type of landfill, 33% is openly dumped, 19% undergoes materials recovery through recycling and composted and 11% is treated through modern incineration.

While developed countries have been emphasizing sorting and recycling for the past decade and therefore have better recycling and recyclability rates than developing countries, the results are not so great. In 2016, in Europe, about 60% of discarded materials were either put in a landfill or incinerated while only 40% were recycled or reused.

Thus, despite an improvement in recycling rates in Europe over the last ten to twenty years, recycling of certain materials is still low: the recycling rate of electrical and electronic waste and plastics was just over 40% in 2016. In addition, manufacturers make very little use of recycled materials in their products: on average only 12% of material resources used in the EU in 2016 came from recycled products and recovered materials - thus saving extraction of primary raw materials.

Facing these disappointing figures, it is urgent to review the way we produce in order to ensure better product recyclability, right from the design stage, but also better sorting and a better recycling rate. This will allow the development of a real market for secondary raw materials, thus limiting the environmental impact of manufacturing production, and in particular the carbon footprint.

Indeed, the manufacturing and transport of products contribute strongly to global warming, even though the carbon budget we have at our disposal is limited if we want to limit global warming to 1.5°C in 2100, in accordance with the Paris Agreement. Respecting this carbon budget implies a reduction of global CO2 emissions, either through products that consume less energy and natural resources or through a decrease in our production and consumption of goods.

The Circular Economy can be a great tool to limit global warming.

Circular Economy: a tool to fight against climate change

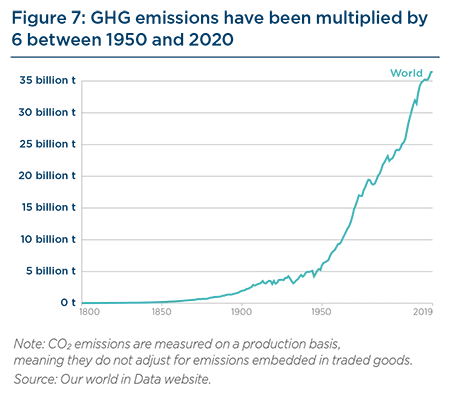

The industrial revolution, from 1850, marks the beginning of the increase of CO2 emissions in the atmosphere. This increase will not stop, even if it may stop during certain economic crises (the two world wars, the oil shocks of the 1970s, the covid crisis in 2020, etc.). Between 1950 and 2020, CO2 emissions in the atmosphere have increased from 6 billion tons to 36 billion tons, i.e. a multiplication by 6 in 60 years (and a multiplication by 18 compared to 1900)!

This increase in CO2 emissions into the atmosphere is directly linked to human activities and in particular to industrial and manufacturing production, the third most emitting sector according to the International Energy Agency (IEA).

The industrial and consumption choices we have made and continue to make, the linearity of our economy based on the principle “extract, produce, consume, throw away” explain this increase in CO2 emissions and global warming.

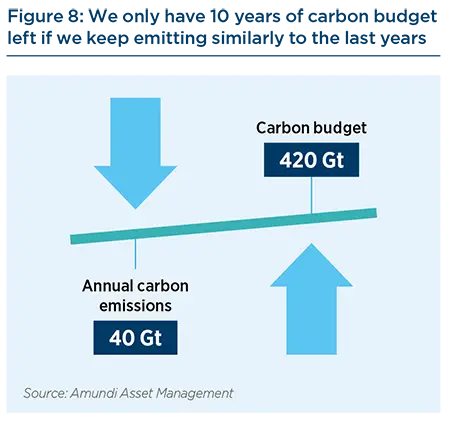

In order to limit global warming to 1.5°C, the International Panel on Climate Change (IPCC) has defined the carbon budget that we can still spend in its latest report: “As of January 1, 2018, we had 420 gigatonnes of CO2 remaining in our "budget" if we want to have a 67% chance of remaining under the 1.5° temperature increase by 2100”6 … while, as said earlier, we emit about 40 gigatonnes of CO2 every year, which means that our CO2 budget associated with 1.5 °C of warming will be exhausted by the end of the 2020’s if emissions remain on the current level of the late 2010s.

Beyond 2°C, scientists estimate that the consequences for the planet's habitability will be major.7

This is why we need to cut drastically our CO2 emissions and for doing so, we need to imagine a new economic model in which producing and consuming is less emissive.

The Circular Economy, by making possible to limit the extraction of natural resources, by limiting production thanks to the extension of the lifespan of products and by allowing better recycling of materials, can play a major role in achieving the climate objectives.

Decarbonisation of energy is necessary, but insufficient to meet climate goals as 45% of CO2 emissions are directly linked to the production of goods and the management of land. Consequently, a thorough transformation is needed in the way we produce and use goods. Besides, as seen earlier, the demand in goods and food will increase in the next decades because of the population growth and will have major consequences in terms of CO2 emissions if we do business as usual.

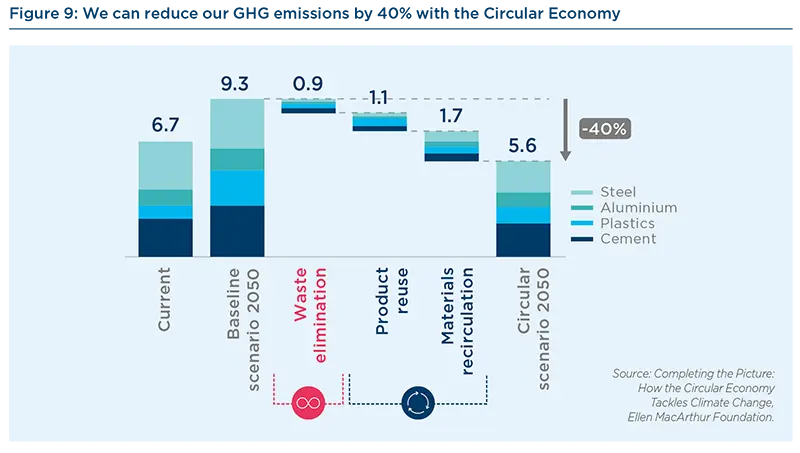

A study by the Ellen MacArthur Foundation8 disclosed in 2019 demonstrates that applying Circular Economy strategies in just five key areas (cement, aluminium, steel, plastics, and food) can eliminate more than 40% of the remaining emissions from the production of goods – 3.7 billions tonnes of CO2 equivalent in 2050 – which equals to cutting current emissions from all transport to zero.

The paper says that “in industry, this transformation can be achieved by substantially increasing the use rates of assets, such as buildings and vehicles, and recycling the materials used to make them. This reduces the demand for virgin steel, aluminium, cement, and plastics, and the emissions associated with their production. In the food system, using regenerative agriculture practices and designing out waste along the whole value chain serve to sequester carbon in the soil and avoid emissions related to uneaten food and unused by-products”.

The paper explains that three main factors can help reduce CO2 emissions due to good manufacturing for the four key materials production, which are steel, aluminium, plastics and cement:

- Waste elimination can help reduce 0.9 bn tonnes of CO2 per year (-9.6%): this is possible through material efficient designs for buildings, industrialised construction processes and ligthweighting designs for vehicles. This allows to reduce the amount of material input in products and assets, and reduce waste generation during construction;

- Product reuse can help reduce 1.1 bn tonnes of CO2 per year (-12%): new business-models such as renting, sharing and pay-per-use can increase the use of products and extend the products’ longevity through reuse, refurbishment and remanufacturing. That way, the need for new products and end-of-life treatments decrease. The need for virgin materials, such as steel, plastics, cement and aluminium decrease as well so do the CO2 emissions;

- Materials recirculation can help reduce 1.7 bn tonnes of CO2 per year (-18%): new business models that consist in collecting, sorting and recycling activities help reduce the CO2 emissions as well. The increase of recycling rates allow to decrease the demand in virgin materials, which helps reducing emissions from production and end-of-life incineration by using less energy-intensigve facilities compared to the production of virgin materials.

Our planet boundaries and climate change force us to review our economic linear model and to replace it by a circular model that will allow to extract less materials from Earth, to better use the products we have at our disposal and to better recycle them. As identified by the EU Green Deal and the New Circular Economy Action Plan, our industry must change.

In the second part of this report, we will analyze how four sectors - Electronics and ICT, Batteries and vehicles, Textiles and Construction and buildings - are facing the new challenges of the Circular Economy and how they are trying to implement it.

Ready, set, go: 4 sectors in the race to the Circular Economy

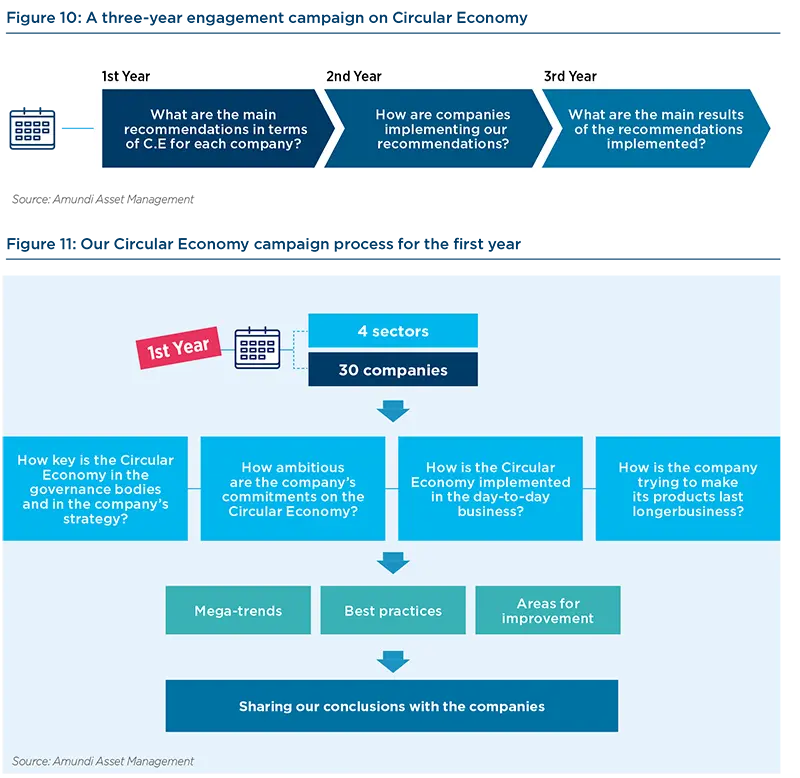

Launch of an engagement campaign on Circular Economy to better assess companies’ maturity on the subject

In 2020, we launched a three-year engagement with four out of the seven most intensive resources sectors identified by the EU:

- Batteries and vehicles;

- Construction and buildings;

- Electronics and ICT;

- Textiles.

About 30 companies based all over the world (USA, Europe, Asia mainly) answered positively to our proposal to engage about Circular Economy.

In order to assess companies, we have developed a proprietary evaluation tool based on four questions:

- How key is the Circular Economy in the governance bodies and in the company’s strategy?

- How ambitious are the company’s commitments on the Circular Economy?

- How is the Circular Economy implemented in the day-to-day business?

- How is the company trying to make its products last longer?

This tool has allowed to assess all companies and to compare them within their sector to highlight mega trends, define best practices and identify areas of improvement.

We have shared the results of this first year of engagement with companies and provided them recommendations. These recommendations will be the foundation of our engagements in the next two years.

Conclusion

The need to combat climate change will profoundly change our society in the coming years and will change the business models of companies. Companies will have to integrate new constraints to limit the environmental impacts of their activities. They will therefore have to identify and assess their environmental impacts in order to find remedial solutions or imagine new ways of doing business.

The Circular Economy can be one of the answers to limit negative environmental impacts. By focusing on the use of goods and not on the good itself and by improving the environmental profile of products - thanks to the economy of functionality, the extension of the lifespan, eco-design, etc. - the Circular Economy makes it possible to reduce our consumption of raw materials and goods and thus to limit our impact on Nature and on global warming.

The commitment we have carried out with four sectors and nearly thirty companies confirms that the Circular Economy is a relevant and necessary response for all sectors. However, the answers to be provided are diverse and some pillars may be more prevalent in some sectors.

The level of knowledge of the Circular Economy remains very variable depending on the sector. The companies interviewed still too often reduce the Circular Economy to waste management alone. Companies still need to complete their knowledge of this concept, especially in order to integrate it from their R&D and thus consider the whole life cycle of the product from its creation to its treatment as waste, including the possibility of extending its life span (simplification of repair, dismantling, etc.).

The implementation of the concept in the four sectors studied also varies from one sector to another. We found that B-to-B companies (Auto, Electronics and ICT, Fashion) are ahead in comparison with the construction sectors. The reasons are different: twenty-year-old regulations for the automotive sector and a rethinking of the business model (switch from internal combustion engines to electric), increasing regulations and repeated scandals that have led to court sentences for certain practices for the Electronics and ICT sector, and increased ecological awareness for the fashion sector. The construction sectors remains behind because the renewal rate of its products is much lower than for the three other sectors and it has to manage an ageing building stock which has not been designed with the principles of the Circular Economy. The integration of the Circular Economy is more difficult in a sector where goods last several decades than for products that are manufactured and renewed almost annually.

However, our study has shown that the integration of the Circular Economy by companies has accelerated over the last five years. European regulation is obviously playing an important role which should not be denied since the Circular Economy is one of the pillars of the New Green Deal promoted by the EU to reduce its CO2 emissions by 55% by 2030 and become a carbon neutral continent by 2050. However, companies will have to confirm that their good intentions and the pilot projects they put forward are turned into action and deployed on a large scale.

See you in two years' time to make sure that the companies' promises are implemented and evaluated again!

_______________

1. https://www.ellenmacarthurfoundation.org/circular-economy/what-is-the-circular-economy

2. https://ec.europa.eu/growth/industry/sustainability/circular-economy_en

3. The date when humanity’s demand for ecological resources and services exceeds what Earth can regenerate in that year in a given year.

4. If we exclude 2020 for which the Earth Overshoot Day was on August, 29th because of the sudden stop due to covid-19.

5. https://openknowledge.worldbank.org/handle/10986/30317

6. https://www.ipcc.ch/site/assets/uploads/sites/2/2019/06/SR15_Full_Report_Low_Res.pdf

7. Rapport GIEC 2018.

8. https://circulareconomy.europa.eu/platform/sites/default/files/emf_completing_the_picture.pdf

Authors