Summary

Introduction and aims

After averting a 1929-style global depression in the wake of the Lehman collapse in 2008, central banks in key economies have faced the Herculean task of unwinding their crisis-era emergency measures, involving zero-bound interest rates and large-scale asset purchases.

10 years on, advanced economies have continued to operate below their natural speed limits. QE has reached the point of diminishing returns, while denting the credibility of its principal architects.

In June 2017, former US Federal Reserve Chair Janet Yellen mused that quantitative tightening in terms of balance sheet normalisation would be like “watching paint dry”.

Yet, while the paint was still drying, the Fed was back in panic mode in January 2019, after the stock markets’ cardiac arrest in late 2018 was blamed on the Fed’s rising rates and shrinking balance sheet. T

The Fed duly performed a sharp U-turn barely a month after Chairman Jerome Powell had proclaimed that quantitative tightening “was on autopilot”.

The Fed’s rate-hiking cycle has now been reversed, as recessionary red flags flutter in the global economy. The European Central Bank has followed suit.

A new era of QE beckons.

It is time, therefore, to perform a stocktake on the effect QE has had on pension plans so far and how their asset allocation approaches are likely to change as QE evolves into its next round.

This report covers three questions:

What has been the impact of previous rounds of QE on the financial viability of pension plans? Where can they find decent returns in this new era of policy reversal? What business model changes will become essential in the process?

These questions were pursued in two separate pan-European surveys.

The primary one covered 153 pension plans; the secondary one covered 38 pension consultants. This report focuses on the first one and uses the second one to validate the key data points.

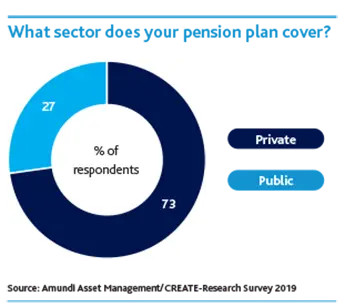

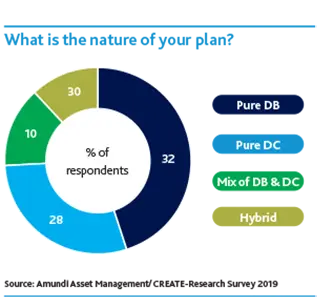

Pensions plans participating in the first survey had €1.88tn in assets under management. Their background details are given in the figure below.

Those in the second survey had €1.4tn in assets under advisement. Data from both sets are appropriately labelled in this report.

The survey results were bolstered by structured interviews with 30 senior executives from the two groups to obtain deeper insights and foresights.

The rest of this section presents the survey highlights, their three headline findings and the four themes that support them.

|

|

To find out more, download the full paper

Authors