Summary

Key Insights

SPACs (Special Purpose Acquisition Company) are companies created and listed on an exchange with the purpose of buying a growth company later. SPACs were derived as an easy way for companies to go public and avoid a long and sometimes difficult quotation process. SPACs are not new, but they have become very popular over the last couple of years. The abundant market liquidity and the return of a pro-risk environment, after the worst of the COVID crisis, have contributed to the growth of the market and to the rising euphoria that has benefitted SPACs.

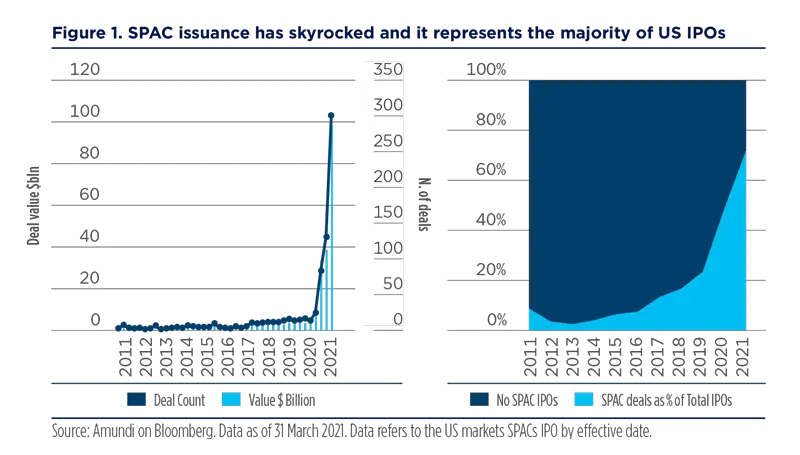

After a record year in 2020, in Q1 2021 the IPOs of almost 300 SPACs raised nearly $100 billion surpassing the overall amount recorded in 2020 and now represents over two thirds of the total value of IPOs in the US market. Amid great market euphoria and spectacular growth, the SPACs phenomenon has attracted many investors. Some sponsors have also involved celebrities1 in deals and their presence has further driven appetite among retail investors, who are not always capable of understanding the structure, costs and risks associated with SPACs.

Most recently, SPACs have made the news headlines as their extraordinary growth has come under pressure. The fact that some SPAC mergers announced didn’t come out as expected has put pressure on their performance, with the IPO SPAC index in bear territory (with losses above 20% since their peak), despite a positive YTD performance for the overall market.

The SPACs phenomenon is now reaching a tipping point. The already mentioned resetting of market performance comes at a time of greater scrutiny from the Securities and Exchange Commission (SEC) that has already started to issue some warnings for investors and is questioning some SPAC practices. The SEC intervention is further freezing new IPOs and giving time to the overall SPAC business to reassess the way forward.

So far, SPACs have most benefitted sponsors and investors with a short-term horizon (arbitragers) and investment banks that earn fees in the IPO and merger process. The excess market euphoria, in fact, has driven price appreciation in advance of mergers, while post mergers performance has been more disappointing therefore hurting long-term investors. The Q1 2021 trend suggests that some excesses are being cleaned up and investors are becoming more cautious and selective. This is leading to rising divergences: SPACs with excessive pre-merger performance driven by rumours are correcting, while the most successful SPAC mergers are delivering positive performances.

In our view, this tendency will further strengthen over the next few months as more than 400 SPACs look for target companies to merge and investors start to be more nervous, looking for performance as with rising yields, bond market alternatives become more appealing (compared with parking money in a SPAC and waiting for a deal).

We believe cautiousness should remain at the forefront for the time being, as the market goes through this phase of maturation, in particular among retail investors. From a long-term investor’s perspective, while we recognise some benefits of SPACs for allowing a faster entrance to the market and a wider spectrum of companies that can go public, we believe that the current structure of SPACs favours more short-term speculative trades. It is less favourable for fundamental investors who look at business models, growth perspectives and at a company’s ESG (Environmental, Social and Governance) profile to build an investment case.

At the end of this transition process, we believe that SPACs will be more specialised and will provide higher visibility on sectors of target companies and better financial disclosure. All these improvements will make the SPAC market more resilient and mature and potentially more appealing for long-term investors.

This is the end of SPAC excess and the evolution towards a more mature and specialised market. In this transition process, divergences in fortune of SPACs will further intensify.

SPACs: the GOOD, the BAD and the UGLY

SPACs (Special Purpose Acquisition Company) have been around for almost three decades2, but their popularity has risen dramatically in recent years.

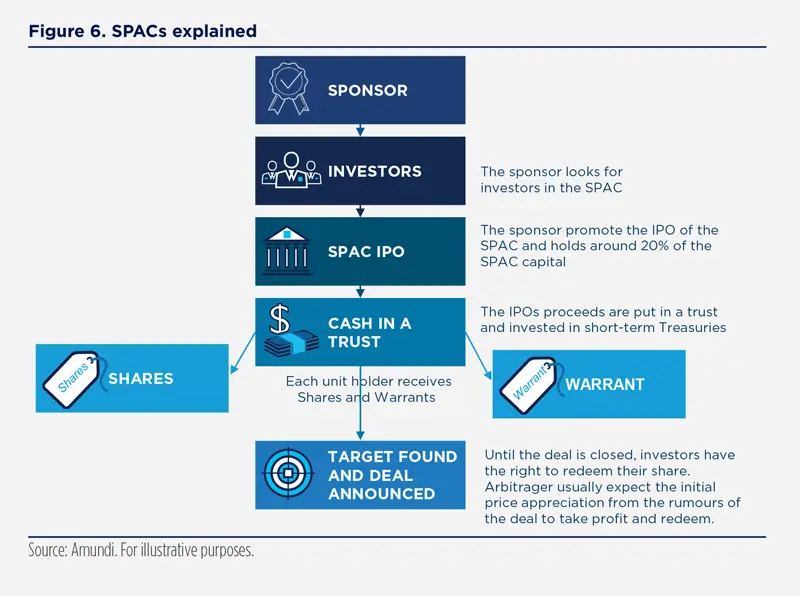

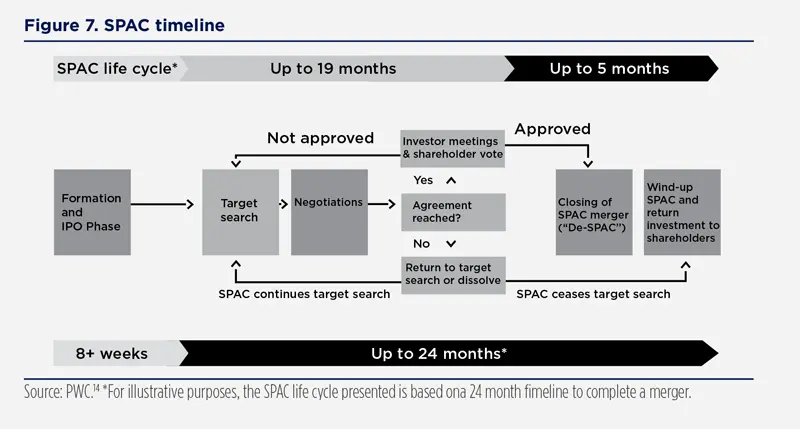

A SPAC is a company created with the purpose of going through an IPO (Initial Public Offering) and raising capital in order to buy a target company within a pre-set period (usually 18 to 24 months). Given this structure, a SPAC is usually referred to as a “Blank Check” company as, at the time of listing, it does not have any specific commercial activity and there is no visibility on the future target company (for further information on SPACs functionality see the Appendix at the end of this document).

SPACs have recently made the news headlines as their volume has skyrocketed since 2020. In fact, in Q1 2021 about 300 SPACs were launched in the US, raising almost $100 billion and surpassing the overall amount raised in 2020, that was already a record year. Not only have the volumes of SPACs and the number of deals been growing, but they have also become a large portion of US IPOs, accounting for 72% of the number of IPOs in Q1 2021 and 66% of their value.

The fact that some hedge funds and bank veterans have launched SPACs has further reinforced the trend and the visibility of this type of instrument and has also attracted some less experienced players into the arena.

SPACs certainly offer some advantages for companies that wish to go public and for investors looking for investments with potential growth similar to private-equity-type targets, but they are also raising some concerns that investors should consider.

The GOOD: the four main benefits of SPACs for companies and investors

|

SPACs offer a faster and easier way to go public and with the potential to value a company on the basis of future projections and with a fixed valuation.

Investors can benefit from a wider universe of high growth global companies that are listed on an exchange and participate in their growth.

They are further incentivised by the usual presence of warrants issued with shares and the possibility to redeem before a merger occurs.

The BAD: the four main criticisms to SPACs

|

Most criticisms of SPAC are particularly relevant for retail investors. The fact that at launch SPACs are blank check companies, and that retail investors may be tempted to enter the market on the basis of excess euphoria driven by market rumours or by celebrity involvement, is a key risk that the SEC has recently highlighted.

Regarding a SPAC’s structure, there could be a potential conflict of interest around a SPAC timeline and costs may be higher than expected due to dilution effects. These are all elements that investors should consider when investing in these instruments.

The UGLY: the four rising trends challenging the SPACs boom

|

The SEC has started to scrutinise SPACs following a rise in litigation. Some recent actions also focus on financial disclosure practices and the accounting treatment of warrants. These actions might cool down the recent boom in SPAC IPOs.

More than 400 SPACs are looking for target companies to merge with. The terms of mergers and target companies will be under the spotlight as investors are starting to look for performance to materialise from their SPAC investments.

SPAC performance increasingly under pressure

With the record high volume of blank check companies entering the market recently there are many voices suggesting a SPAC bubble may be about to burst. Actually, there are some signs that SPACs have reached a tipping point, particularly when looking at performances.

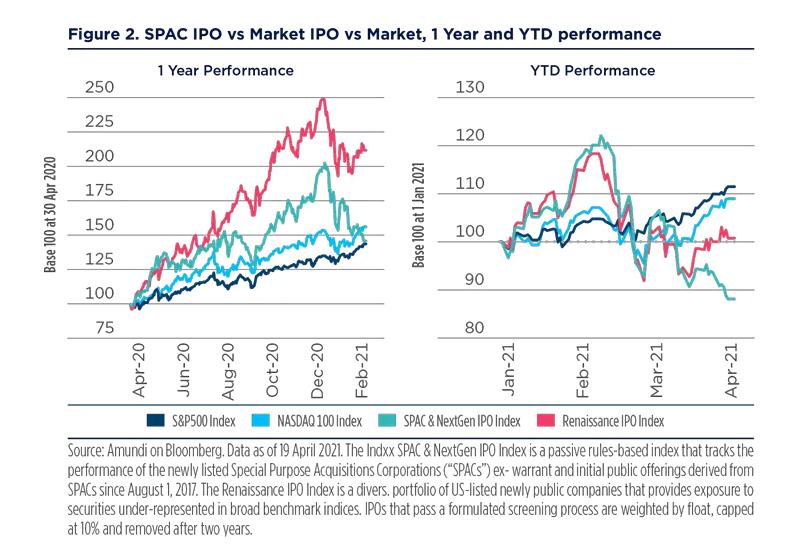

We have compared the general market performance (see Figure 2) of the US IPO index vs the SPAC IPO Index and the general US market performance represented by the S&P500 and the technology sector via the NASDAQ index over the past year and since the start of 2021. Over the last 12 months all indices had positive returns, with an upward trend being pronounced until mid-February 2021. Since then, despite the still positive performance of the overall market (S&P500 and NASDAQ indexes), the IPOs indices started to underperform. Most recently, in April, the IPO index recovered its YTD losses, while the SPAC IPO index remained in bear territory, with a loss from its peak at -28% (at April 19th).

This recent underperform is putting pressure on SPACs to deliver on their promises.

SPACs have reached a tipping point. A first signal comes from performance. In fact, despite still positive performance for the market and a fast recovery for the overall IPO index, the SPAC IPO index has not shown any sign of improvement and remains in bear territory.

One of the major criticisms recently posed about SPACs relates to their performance being lower in comparison to traditional IPOs.

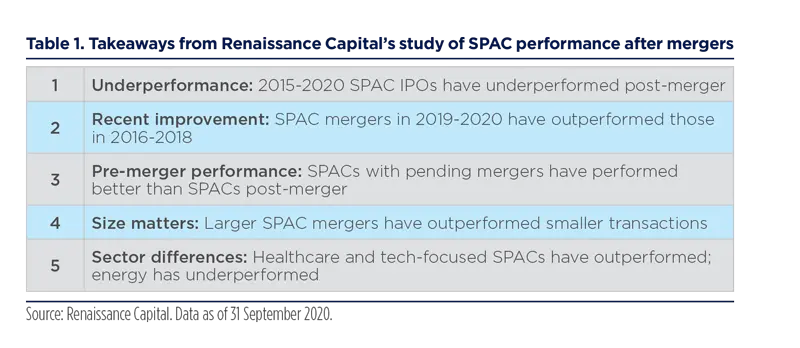

When looking at historical performance, this trend appears to be confirmed by an industry study comparing SPAC returns with average IPO returns11.

Looking at historical studies on SPAC performances vs IPOs there is evidence that SPACs have underperformed, although this trend did improve in 2019-2020.

SPACs performance has mainly benefitted sponsors and arbitragers in the past

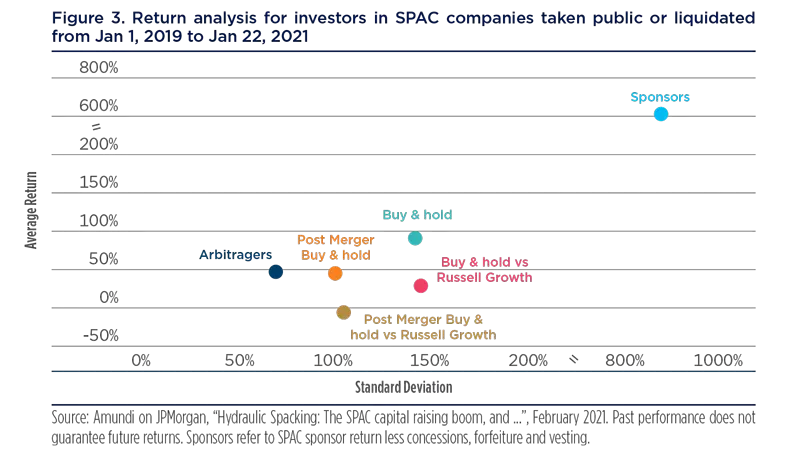

A recent JPMorgan study12 on the performance of SPACs over the last two years has highlighted key differences in the performance experienced by different types of investors. In particular, the key winners have been sponsors, with stellar performance. A second group of investors that benefitted from SPACs have been the so-called “SPAC Arb investors”. They are usually hedge funds or other institutional investors that opt to redeem their shares before the merger and that also sell the warrant before the merger. While the performance of this second group of investors has been much lower compared to sponsors, they have usually made very positive gains with low variability compared to the results of other investor groups and within a shorter horizon, as they have held their shares just up to the merger. Performance for buy and hold investors has also generally been quite good overall, although less so when compared to the performance of the Russell 2000 Growth Index. Finally, the investors that experienced the worst returns, also considering the variability of returns (standard deviation within the investment group) have been those that entered “buy & hold” post-merger.

SPACs have overall delivered positive performance for all investors over the last two years. Sponsors have been the main gainers, arbitragers have been the ones with the best risk- adjusted return profile, while investors that entered post-merger have benefitted the least.

A maturing industry can help improve SPAC performance, including post-merger

The announcement that the Singapore-based Grab Holdings is going to become the largest ever SPAC merger with a value of almost $40 billion is an illustration of the potential that SPACs offer. This company, called Southeast Asia Uber, is a highly promising business, that otherwise would have been unlikely to have made its way into a US public market.

The case study of Grab is also interesting regarding the performance behaviour of Altimeter Growth Corp., the SPAC entering the deal. In fact, the shares of Altimeter rose on rumours of the possible announcement, but far below the movement seen in the past in relation to the pre-announcement phases of other SPACs. Recent cases of preannouncement rises resulted in losses ex-post and investors are therefore starting to be more cautious compared to past excess euphoria.

In fact, the maturing of the market is helping to clean up some of this excess and may lead to improvements in SPAC performance. In Q1 2021, according to PWC, the SPACs that completed their mergers shown a healthy return of 27%, outperforming the IPO sector returns and more than the market return in general. So, this means that the overall negative performance experienced by the market (see previous chapter and Figure 2) may be due to the reassessment of excess performance in pre-merger phases (representing the majority of the market at the moment), while in contrast, successful mergers proved to be profitable for investors.

Price action in Q1 2021 showed that the excess euphoria in the pre-merges phase is dampening, while companies that actually deliver mergers are enjoying positive performance.

The reassessment of the industry is likely to continue, as new SPAC IPOs are taking a pause. SPAC IPOs are cooling down, with new IPOs announced in the US literally falling to 0 in April, after a meagre 14 in March versus more than 200 in January and February combined. We believe this trend is likely to continue given the recent intervention from the SEC. In particular, the recent announcement on the revision of the treatment of warrants is further freezing new IPOs, as advisers and lawyers are waiting for more clarity on rules going forward.

We also welcome the spotlight from the SEC on SPACs and on the potentially misleading projections made at the time of the mergers13 as this should push further in the direction of greater responsibility in terms of financial disclosure. All these measures should help the maturing process and lead to SPACs increasingly benefiting long-term buy and hold investors.

Investors should increase scrutiny in SPAC sponsors and structures

In general, we believe that investors still willing to participate in the SPAC business should be very careful. They should allocate only a marginal part of their portfolio to SPACs, do proper due diligence on the sponsors and the SPAC structure and carefully assess the possibility of redeeming before a merger if it is not a valuable one.

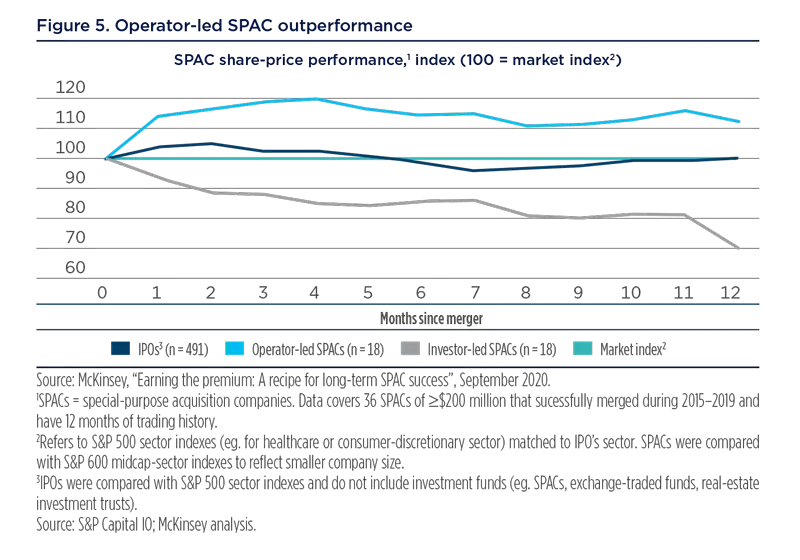

Some research in the direction of greater scrutiny about how SPACs are built already points to possible higher performance and lower risk depending on some features of the SPAC. A recent study by McKinsey shows that what they call “Operator-led” SPACs (SPACs whose leaders have significant operating experience, versus purely financial or investment experience) enjoyed better performance compared to the overall market and other SPACs. This is mainly driven by the fact that these experts tend to operate on a specific industry that they are highly knowledgeable about and they also take on roles in the post-merger company (chair or vice chair role), putting their expertise at the service of the newly formed company.

Moving ahead investors should scrutinise in depth the SPAC structure and its sponsors’ expertise. We share the view from McKinsey that more specialised SPAC sponsors, who take an active role postmerger, will likely keep a competitive advantage.

Conclusion

The current reassessment of the SPAC phenomenon is accelerating further due to the rising focus from the SEC. This will likely lead to a pause in new filings and some changes in current market practices. The most expert sponsors will emerge as winners, while inexperienced ones, that entered the market on the wave of the SPAC success, will be challenged.

In this maturing process, we believe SPACs will survive and the market will become more efficient, but while this process unfolds, investors (particularly retail ones) should be very cautious.

Once current market excess is reabsorbed, the SPAC market will likely end up being more specialised, providing some higher visibility on industries of focus and with better practices in terms of the financial disclosure of target companies. Until then prudence is paramount, but we should not move from one excess to another, demonising an investment vehicle that has demonstrated strong potential.

After the current clean-up of market excess, the most expert sponsors will emerge as winners, while inexperienced ones, that entered the market on the wave of the SPAC success, will be challenged. Until this process is over investors should be cautious on SPACs.

APPENDIX - SPACs at a glance

The role of the SPAC sponsor

In the creation of a SPAC, sponsors play a key role. The Sponsor can be one or more experienced executives in a certain industry, a company or even private equity or hedge fund. They provide part of the initial capital and, as remuneration for their activity, they gain a higher share of the SPAC, usually around 20% and additional warrants. Their role is initially to promote the SPAC to investors for the IPO and subsequently to search for potential target companies. They should also commit to the SPAC for a certain timehorizon, as their promoted shares usually can’t be sold for a period of one year after the merger or they can sell them if the share price reaches a certain target.

The SPAC IPO process

The SPAC IPO is usually quite straightforward; the documentation on the company mainly concerns the structure of the SPAC as there is no business data to be shown.

The SPAC initial price is usually set at $10 per unit, and the IPO proceeds are held in a trust and invested in short-term Treasuries until the company finds a target to acquire.

SPAC warrants

The unit price of a SPAC is usually set at $10 and it includes a warrant that allows the investors to purchase a share of the stock. The warrant for example can be exercisable at $11.50 per share and it can have a specific horizon; for example 30 days after the merger transaction or twelve months after the SPAC IPO.

The SPAC timeline

The SPAC has usually a maximum of 24 months to find a target to buy and gain the approval from the shareholders for the merger, otherwise it will have to return the capital to the shareholders.

SPAC performance

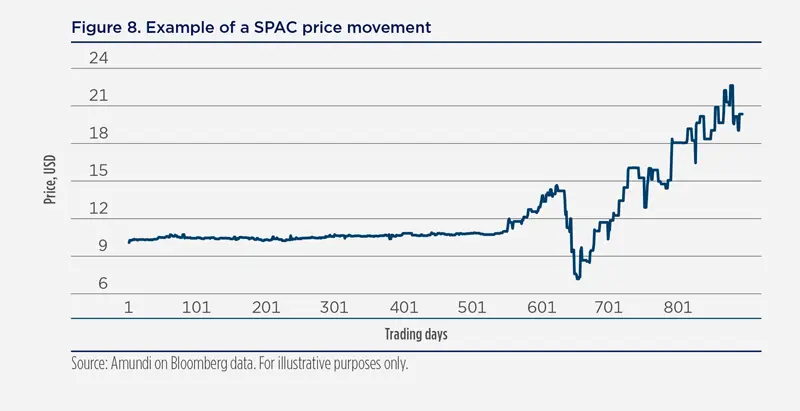

SPAC performance after IPO differs quite significantly from a traditional IPO. In fact, SPACs initially trade close to a short-term Treasury as the company has not given any detail yet on the possible acquisition. In contrast, a traditional IPO will deliver its performance directly upon listing and may be very volatile just after.

After this initial phase, once the company enter negotiations with a target company, SPAC prices start to price in the possible acquisition. After the merger is effective, the price will move, as with any traditional listed company, in line with the company news and the business results announced.

Definitions

- Celebrities include Shaquille O’Neal, Paul Ryan, Colin Kaepernick, Jennifer Lopez, Jay-Z, Serena Williams.

- SPACs were invented by investment banker David Nussbaum and lawyer David Miller in 1993.

- https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-alerts/celebrity

- https://ore.exeter.ac.uk/repository/bitstream/handle/10871/25163/Manuscript_4.pdf?sequence=1&isAllowed=n

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3720919

https://corpgov.law.harvard.edu/2020/11/19/asoberlookatspacs/#:~:text=The%20primary%20source%20of%20SPACs%E2%80%99%20high%20cost%20and,do%20not%20contribute%20cash%20to%20the%20eventual%20merger. - https://www.sec.gov/corpfin/disclosure-special-purpose-acquisition-companies

- https://www.sec.gov/news/public-statement/accounting-reporting-warrants-issued-spacs?utm_medium=email&utm_source=govdelivery

- https://www.ft.com/content/c94f51f5-c042-42a6-8ba1-81b5672d2820

- https://www.wsj.com/articles/short-sellers-boost-bets-against-spacs-11615714200

Source: https://www.spacresearch.com/ Data as of 13 April 2020. - https://www.ft.com/content/bacdf86f-e786-4439-966e-f5958adb1c59

- https://www.renaissancecapital.com/IPO-Center/News/71816/Updated-SPAC-returns-fall-short-of-traditional-IPO-returns-on-average

- Source: JPMorgan, “Hydraulic Spacking: The SPAC capital raising boom, and …” February 2021.

- https://www.sec.gov/news/public-statement/spacs-ipos-liability-risk-under-securities-laws

- https://www.pwc.com/us/en/services/audit-assurance/accounting-advisory/spac merger.html#:~:text=Special%20purpose%20acquisition%20companies%20(SPACs)%20have%20become%20a%20preferred%20way,sponsors%20to%20take%20companies%20public.&text=Subsequently%2C%20an%20operating%20company%20can,of%20executing%20its%20own%20IPO

Authors