Summary

- Optimism was definitely behind the respectable performance registered by risky assets in the last quarter. However, the economic backdrop does not look overly positive. On the price levels side, US headline inflation is receding, although the core measure - more important for monetary policy decisions - is proving to be stickier. The latest European and UK inflation numbers signal that price growth is cooling.

- Central banks (CB) are possibly winning the battle against inflation, however, what we need to gauge carefully is the extent to which the economy was damaged by restrictive policies. On the growth side, our estimates are pointing towards a mild recession in the US and a slowdown in Europe, mainly driven by tight financial conditions and an unexpectedly weak Chinese stimulus, which the Old Continent economy is linked to.

- We foresee a vigilant Fed in the short-term: rate cuts are possible only if core disinflationary trends materialise. Emerging market (EM) economies are out of sync with developed markets. In fact, CBs in this part of the world are on a more neutral, if not dovish, stance.

- Our long-term model assumptions are characterised by a disorderly energy transition that integrates secular trends and uncertainty, both affecting price dynamics and volatility. Interest rates will normalise in the long-run on upward sloping, albeit flatter, curves.

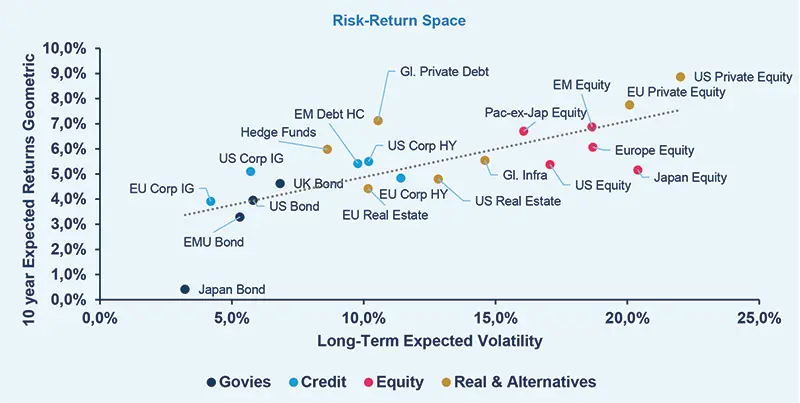

- From a strategic standpoint, high-quality fixed income assets, government bonds, and high-grade credit can deliver attractive returns. This quarter we consolidated our expectations over a 10-year horizon because of improved starting valuations. Equity returns are confirmed modest in the long-run, especially compared to historical norms. Expectations on EM Equity and Pacific ex-Japan Equity have improved, whereas Japan Equity is expected to underperform its peers, also considering risk adjusted returns.

- In the Real and Alternative Assets space, Global Private Debt and Hedge Funds confirm their attractive risk/return trade-off, also towards asset classes with similar levels of risk (High-Yield Credit and Real Estate).

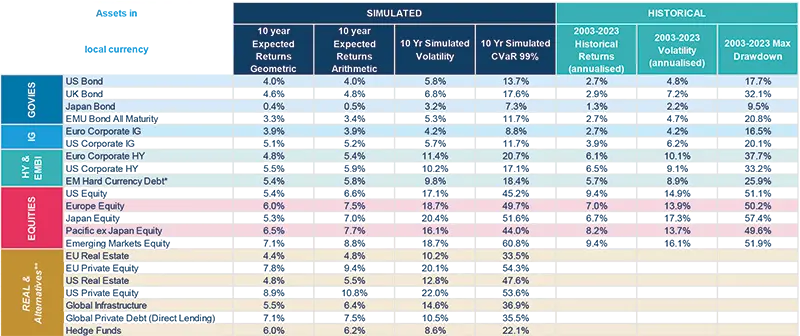

In the table below, we present our simulated forward-looking statistics over a 10-year horizon (expected returns, volatility and CVaR) compared with historical statistics calculated using a 20-year sample. Here, CVaR and max drawdowns represent the expected and historical shortfalls, respectively. We also provide arithmetic average returns, which are used for portfolio optimisation purposes.

*Hard currency USD, **Historical figures on real and alternatives are not available, as our models refer to un-smoothed data if necessary. The arithmetic average returns are derived using the price generated by our simulation engine, CASM. By definition, the arithmetic mean is always greater than or equal to the geometric mean. In particular, higher volatility of returns and higher frequency of returns and/or a longer time horizon will increase the difference between the two measures. Regarding real assets, the table represents the modelling of core/core-plus (moderate risk) real estate and direct lending on the private debt side. The expected returns do not consider the potential alpha, generated by portfolio management that can be significant above all for real and alternative assets.

Asset Class Return Forecasts

Expected returns are calculated using Amundi central scenario assumptions, which include the climate transition. For more detailed information, see: A rocky net zero pathway

Source: Amundi Asset Management CASM Model, Quant Solutions and Amundi Institute Teams. Full source on page 5.

n the chart we present the range of arithmetic expected returns, where we have excluded tail scenarios.

Amid the yield curve uplift, our expectations for government bond returns are still attractive, notwithstanding the dispersion around the central scenario. In particular, we highlight UK bond expected returns dominating the sovereign bond universe (investors should keep in mind the duration mismatch), and Japan Bonds continuing to lag peers.

Credit return forecasts for high-grade assets are in line with government bonds. However, low-quality assets are expected to marginally outperform higher quality assets and present a larger outcome dispersion due to greater intrinsic volatility and default loss assumptions.

On the equity side, we confirm moderate 10-year expected returns between 5% and 7%. However, based on our simulations we cannot exclude the possibility of negative returns: there is a 5% chance for equity returns to be below zero over a 10-year horizon. Our assumptions on equity fundamentals were revised up slightly as a consequence of the developing macroeconomic backdrop. However, expected returns in some regions were offset by more expensive starting valuations, as the US and Japan demonstrate.

Equity-like private assets, are expected to provide investors with close to double digit returns. Real Estate expectations are in line with high quality credit, although the dispersion around the central scenario is materially larger due to the illiquidity and complexities of this asset. Global Private Debt reveals a competitive expected risk-adjusted return, making this asset a convincing alternative to credit-like instruments.

Moving to the medium-term, government yields have increased recently, especially in the short-end of the curve, as markets incorporated recent rate hikes from CBs. Compared to our latest quarterly update, our 5-year returns for fixed income are still below 10-year returns, although much closer. Finally, we still expect equity to provide moderate 5-year returns ranging between 7% and 9%.

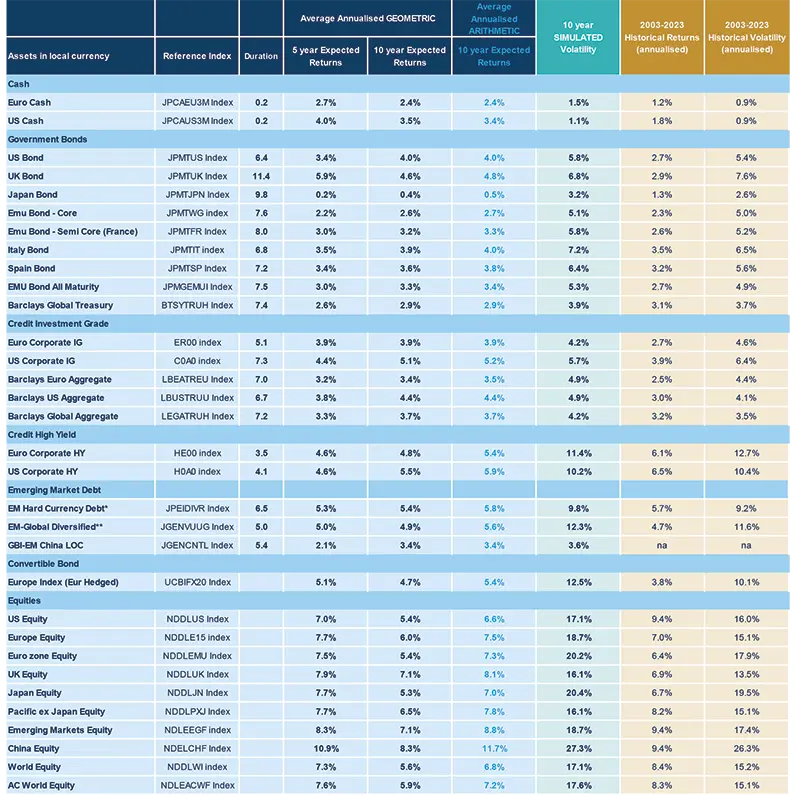

In the following table, we present our annualised return forecasts across different asset classes, calculated as the average of simulated returns over different forward-looking horizons (five- and ten-years). We also report historical figures for annualised returns and volatility calculated over the last 20 years, a sample that includes the two big rises (GFC and Covid-19).

* Hard Currency USD, China Bond starting date is beginning of 2019. ** USD Unhedged, including the USD currency expectation towards EM currencies.

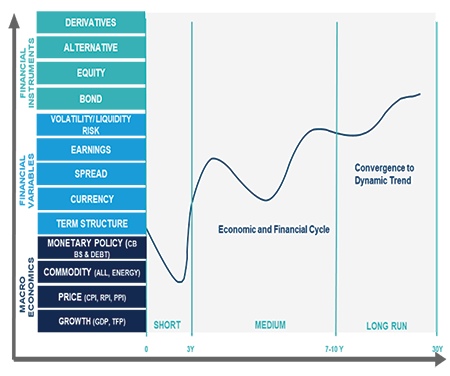

Cascade Asset Simulation Model (CASM)

This medium- and long-term return forecast report is intended to provide some guidance for investor expectations. The time horizon under consideration is 10 years, a timeframe deemed to be appropriate and during which long-term trend factors and issues can reasonably be expected to play out and, therefore, market returns should accurately reflect this information.

Cascade Asset Simulation Model (CASM) is a platform developed by Amundi in collaboration with Cambridge University. CASM combines our short-term financial and economic outlooks. It incorporates medium-term dynamics into a long-term equilibrium, to simulate forward-looking returns for different asset classes over multiple horizons.

CASM generates asset price scenarios and underlying economic and financial factors that determine Amundi’s expected returns. It is a valuable tool for strategic asset allocation and asset-liability management analysis. We estimate model parameters quarterly to incorporate new market data and our short-term outlook. The process for calibrating models that reflect our view of economic and financial market trends is a collaborative process between many teams at Amundi. We reach a consensus for the short-to-medium term outlooks for macro and financial variables for each region under consideration (US, Eurozone core and periphery, UK, Japan, China). The models are calibrated to be consistent with these outlooks and long-run estimates. At each step in the process, results are analyzed against stylized facts and checked for consistency. Price returns are generated using Monte Carlo simulation. Stochastic generation of risk factors and price scenarios allows us to analyze a wide range of possible outcomes and control the uncertainty surrounding these. We can change starting assumptions and see the effect on possible future asset prices. The CASM platform covers macro and financial variables for major regions, in particular the US, UK, Eurozone, Japan, China and Emerging Markets as an aggregate.

The architecture of CASM can be described in two dimensions. The first dimension is a “cascade” of models. Asset and liability price models are composed of market risk factor models. Market risk factor models are made up of macroeconomic models. Initially proposed by Wilkie (1984) and further developed by Dempster et al. (2009), this cascade structure is at the root of the platform’s capability to model linear and non-linear relationships between risk factors, asset prices and financial instruments. The second dimension is a representation of the future evolution of the aforementioned “cascade” effect.

The unique formulation allows us to simulate asset price scenarios that are coherent with the underlying risk factor models. In the short term, CASM blends econometric models and quantitative short-term outlooks from in-house practitioners. In the long term, we assume the market variables are subject to dynamic long-term levels. The short term evolves into a long-run state through the medium-term dynamic driven by business cycle variables.

Sources

Amundi Asset Management CASM Model, Amundi Asset Management Quant Solutions and Amundi Institute Teams, Bloomberg. Data as of 28 April 2023. Macro figures as of latest release. Starting date is 31 March 2023. Figures shown are in local currency. Returns on credit assets are comprehensive of default losses. Expected returns are calculated on Amundi central scenario assumptions, which include climate transition. Regarding real assets, the table represents the modelling of core/core-plus (moderate risk) real estate and direct lending on the private debt side. The expected returns do not consider the potential alpha, generated by portfolio management that can be significant above all for real and alternative assets. Forecasts for annualised returns are based on estimates and reflect subjective judgments and assumptions. These results were achieved by means of a mathematical formula and do not reflect the effect of unforeseen economic and market factors on decision-making. The forecast returns are not necessarily indicative of future performance, which could differ substantially.

Author