Summary

- Main takes from the ECB: European Central Bank (ECB) President Christine Lagarde made it clear that rate cuts aren’t on the table: ‘we did not discuss rate cuts at all’. Lagarde said the ECB shouldn’t ‘lower its guard as inflation tumbles’. Despite positive recent developments, the ECB wants to remain cautious, as she expects an uptick in inflation over the coming months. Wages are the biggest factor. The ECB remains particularly concerned about wage development in a context of falling productivity. This stands in stark contrast to the Federal Reserve (Fed), which is intensely focused on the growth risks associated with keeping rates high for an extended period of time. This divergence is particularly notable given the Euro zone’s weaker economic performance in recent months, and more rapid disinflation compared to the United States. Indeed, monetary policy has impacted the Euro zone’s economy faster than expected, and more is yet to come. Bank’s credit conditions have already tightened significantly. Lending to the area’s companies fell by 0.3% year-on-year in October 2023, marking the first decline since July 2015.

- Future policy prospects: We currently see a first interest rate cut in June 2024, and 125bp rate cuts overall in 2024. However, risks to growth could push the ECB to ease monetary conditions more quickly. The ECB also revised its roll-off plans for the Pandemic Emergency Purchase Programme (PEPP) portfolio, and will start to reduce reinvestments by EUR 7.5bn on average per month in the second half of 2024.

- Main takes from the BoE: The Bank of England (BoE) also kept rates unchanged, showing no intention of deviating from its 'higher for longer' policy stance. Despite encouraging signs from the labour market and the Consumer Price Index trend, the BoE’s forward guidance was also hawkish, leaving the door open for future rate hikes if necessary.

- Market reaction and investment implications: With the Fed in pivot mode, markets remain tilted towards a 'goldilocks' reading of the economic outlook. Sharp movements in core yields complicate the call on duration: current levels support a cautious stance, but an economic slowdown would warrant being more constructive on duration. Corporate credit has benefitted, with value to be found in the Investment Grade (IG) segment, particularly financials. We remain cautious on the more vulnerable parts of High Yield (HY), but there is scope to explore higher rated non-investment grade segments like BB or short maturities across the HY asset class. In Foreign Exchange (FX) markets, the Japanese Yen is expected to benefit from monetary easing in the US, and the Euro and British Pound have also benefitted, but the latter may be weighed down by weak economic data and still-high inflation in the foreseeable future.

Key takeaways from the European Central Bank’s meeting

ECB President Christine Lagarde made it clear that rate cuts aren’t on the table, in stark contrast to the Fed, which is intensely focused on the risks to growth associated with maintaining higher rates for an extended period. This divergence is particularly notable given the Euro zone’s recent weaker economic performance and more rapid disinflation compared to the United States.

Monetary policy has impacted the Euro zone’s economy faster than expected. Tighter financing conditions are dampening demand and we expect this trend will continue. Moreover, bank’s credit conditions have tightened significantly. Lending to the area’s companies fell by 0.3% year-on-year in October 2023, marking the first decline since July 2015.

The ECB remains focused on inflation. Despite positive recent developments, the ECB remains cautious in anticipation of a possible uptick in inflation over the coming months. Wages are the biggest factor to watch, with the ECB concerned about wage development in a context of falling productivity.

Despite positive recent developments, the ECB remains cautious in anticipation of a possible uptick in inflation over the coming months

Policy rate and quantitative tightening expectations in the coming months

In our central scenario, we expect economic activity will be supported by rising real incomes, as people benefit from falling inflation and growing wages. We also believe inflation could pick up again temporarily in the near term, mainly due to base effects. Under this scenario, we expect a first rate cut in June next year, and 125bp rate cuts overall in 2024. However, we are monitoring the risk that rising wages and lower productivity result in lower corporate margins rather than price increases in a low demand environment. Sharper than expected inflation slowdown could push the ECB to ease monetary conditions earlier.

Regarding quantitative tightening (QT), the ECB revised its roll-off plans for the PEPP portfolio. It will start reducing reinvestments by EUR 7.5bn on average per month in the second half of 2024. Ending PEPP reinvestments is really a question of ‘normalisation’. Even though the ECB does not see fragmentation risks, it stated that it would not hesitate to use the tools at its disposal.

Even though the ECB does not see fragmentation risks, it stated that it would not hesitate to use the tools at its disposal.

A view on the Bank of England

The BoE also kept rates unchanged and was possibly the most hawkish, maintaining a cautious stance, showing no sign of deviating from its ‘higher for longer’ policy stance. The decision on rates saw a split vote, as in the central bank’s previous meeting, that was largely expected given softer inflation but weaker-than-consensus growth data. Moreover, the BoE took note of recent encouraging signs from the labour market, and how Consumer Price Index (CPI) inflation fell sharply in October and is expected to remain near current levels around the turn of the year. Its forward guidance was also on the hawkish side, with a bias for tightening, and leaving the door open for another hike mostly to guard against a premature easing of financial conditions.

Implications for fixed income and FX markets moving into 2024

The BoE was possibly the most hawkish, maintaining a cautious stance, showing no signs of deviating from its ‘higher for longer’ policy stance

The ECB and BoE struck a more hawkish tone compared to the Fed, but with the Fed in pivot mode, markets remain tilted towards a ‘goldilocks’ reading of the economic outlook. Sharp movements in core yields complicate the call on duration. Current levels support taking a cautious stance, but an economic slowdown next year would foster the conditions to become more constructive on duration, therefore we maintain a flexible approach.

Corporate credit has benefitted from this phase. There is value to be exploited in the Investment Grade segment, particularly in financials. In fact, whereas higher rates will start to bite particularly lower-rated High Yield names, the IG space remains resilient. While we maintain a cautious stance on the more vulnerable parts of HY, we believe there is scope to explore higher rated non-investment grade segments like BB, where the fundamentals are more guarded or short maturities across the HY universe.

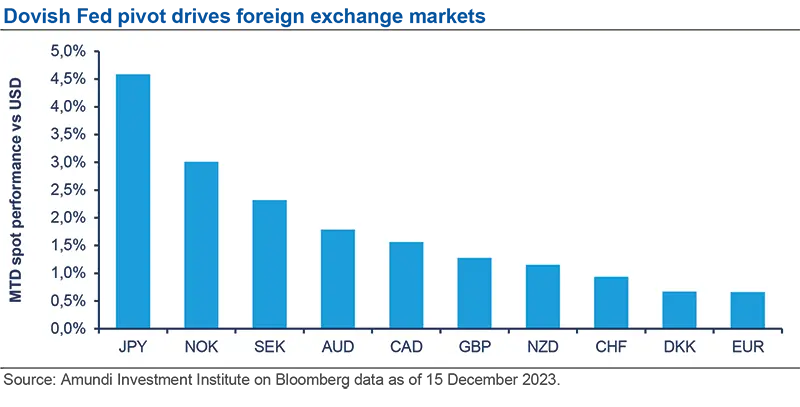

The Fed’s dovish pivot, compared to the ECB and BoE holding tight, have also driven Foreign Exchange markets. Sharp price action on US rates weakened the US dollar (USD) against other major currencies, with a strong rally on the Japanese Yen (JPY). This week’s policy meetings reinforced out conviction of being long JPY against the USD, and supplement a constructive view on Emerging Market FX, which should benefit from monetary easing in the US. The Euro (EUR) and British Pound (GBP) also benefitted from Fed Chair Jerome Powell’s dovish comments, and are trading at their highest levels in the last four months. So far this year, the EUR/USD parity remains in a narrow range between 1.05-1.10, and is still valid. After a good run against the greenback, weak economic data and still-high inflation should weigh on the GBP in the foreseeable future.

Author