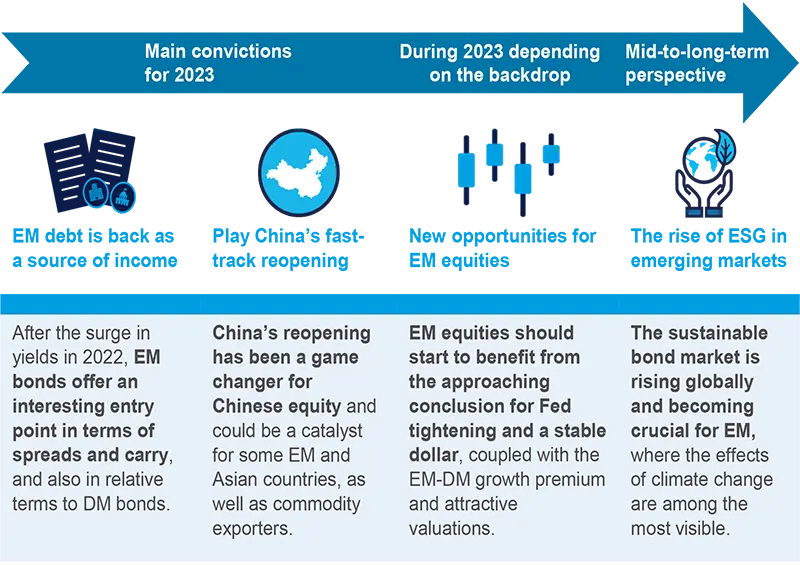

The emerging market comeback

Amid China’s earlier than expected reopening and a downturn in US economic conditions, emerging markets are well positioned to continue outpacing their developed peers for growth in 2023. Discover our experts’ views on investment opportunities across EM regions and asset classes.